Market Forecast

Autumn 2025

Planning Ahead for Autumn Price Increases

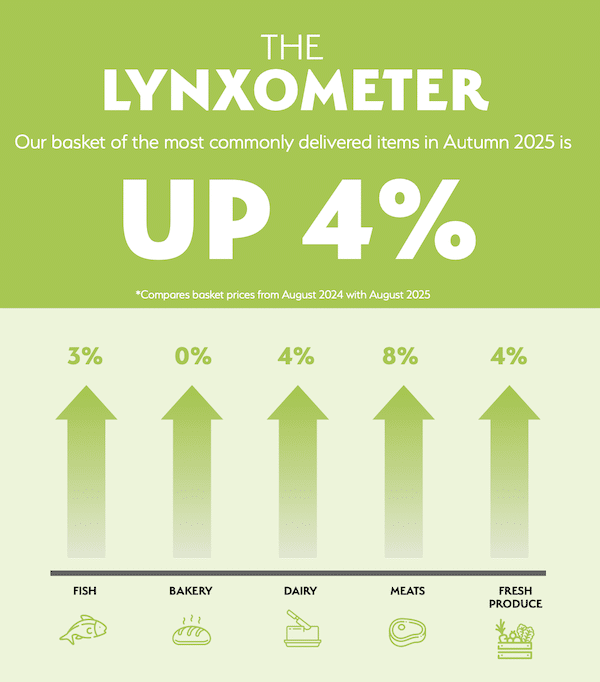

With the inflation rate forecast to stay significantly above the Bank of England’s 2% target across the autumn and into the peak festive season, and food inflation in particular staying high, operators will need to plan carefully for the next few months.

Hospitality businesses don’t need reminding that consumer confidence is fragile, but there are some promising signs, with the ONS reporting an increase in the rate of average wage growth this year. That should mean people feel they have more disposable income when it comes to meeting up with friends and family, as well as making bookings for Christmas.

The other side of the coin is that hospitality running costs are higher due to the National Insurance and Living Wage increases. These costs also affect the supply chain, with most food production being labour intensive, which is a big factor in the food inflation forecast.

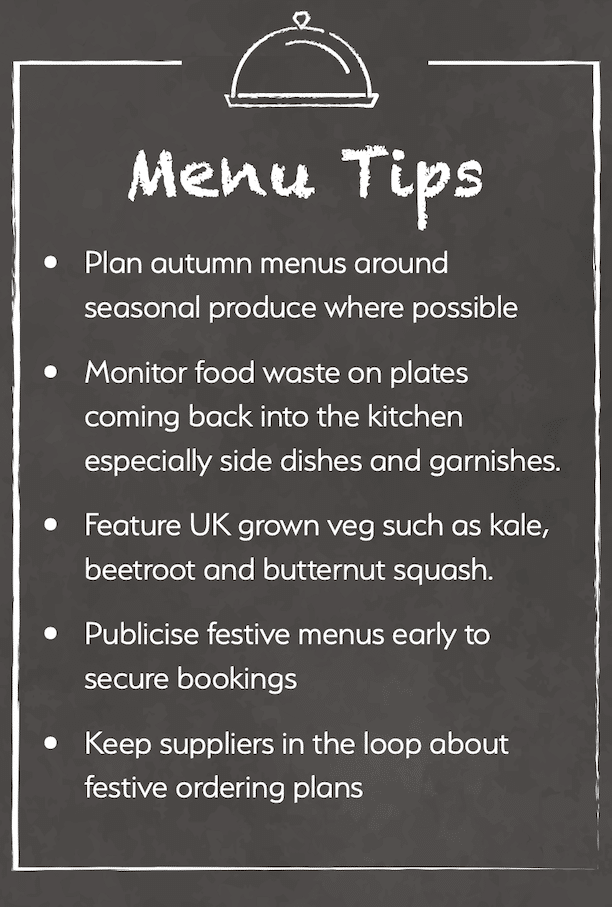

To make the most of the opportunities of autumn and winter trading, operators should plan menus that maximise the use of seasonal produce – at its best in terms of availability, quality and value – and keep food waste to a minimum. Managing these costs can make a significant difference to the bottom line.

As always, suppliers can advise on changing availability, so keep menu descriptions flexible where possible. When it comes to set festive menus, the earlier operators can place orders, the better the value suppliers can offer.

The longer-term forecast is for the food inflation rate to fall below 2% by mid-2026, which should ease the pressure on hospitality budgets next year.

The Good

- Improving consumer confidence

- Peak trading period approaching

- Food inflation should fall in 2026

The Bad

- Higher costs impacting businesses

- Hot summer has affected food production

- Conflict/climate change impacting global economy

Menu Watch

Everyone loves a barbecue, but British chefs and restaurants are adapting traditional US dishes by adding a fusion twist, research into menu trends shows. Mexican, Korean, Thai and Caribbean influences are turning up on barbecue menus, with examples including baby back ribs paired with kimchi and spring onions, cumin-spiced pulled lamb shoulder, and jerk pork belly slices.

Fancy a little drink? As more consumers moderate their alcohol intake, many restaurants are offering a micro-cocktail option on their pre- and post-dinner drinks menus. This allows customers to enjoy the flavour of

a cocktail without over-indulging, or to have more than one with a clear conscience. Mini- martinis, ‘snaquiris’ and pocket negronis have all been seen on drinks lists.

The humble sandwich is making a break from the lunchtime offer to become part of main menus. More operators are offering gourmet hot sandwiches, featuring artisan fillings and home-made breads such as brioche and sourdough. Varieties include patty melts, freshly-filled subs, and sandwich specialities such as the Reuben, a New York favourite made with corned beef, Swiss cheese and sauerkraut.

FRUIT

A range of UK fruit, such as apples, pears and berries, ripened early due to the extended heatwave in the summer. While quality is mainly good, availability may be affected later in the season. A more challenging fruit harvest in parts of Europe will affect manufactured products.

BEEF

UK cattle farmers remain reluctant to expand production due to very high rearing costs. As a result, beef prices continued to increase across the summer and are expected to rise further this autumn, as retailers compete for available supplies. This leaves hospitality operators in the challenging position of dealing with higher prices and lower availability as the peak season approaches.

COFFEE

While coffee prices have risen sharply, forecasts for supplies on the global markets have improved a little, due to better-than-expected harvests. The impact of tariffs on US imports also means coffee suppliers are looking at different markets, which could benefit UK hospitality operators able to shop around for the best deals on coffee.

OILS

Global production of cooking oils remains volatile, driven by factors ranging from the continuing impact of the Ukrainian war on sunflower oil, to the impact of climate change on olive oil production around the Mediterranean. This impacts the price of oil as well as many manufactured products.

DAIRY

Dairy prices have been high for much of this year, and producers have warned that higher costs in areas such as cattle feed, as well as a shortage of labour, will continue to have an impact. Butter has seen sharp price increases, and the challenges also affect prices of manufactured products which use dairy, as well as cheese.

FISH AND SEAFOOD

Cooler waters in autumn create good conditions for a wide range of fish and seafood, with species including mackerel, coley, plaice, lemon sole and mussels from UK waters expected to be good value. Winter is more challenging for the UK fishing fleet. Suppliers can advise on availability, as well as offer some species in frozen and vacuum packs across the winter.

POULTRY

Prices have been more stable recently, making chicken dishes a reliable option for operators when planning menus. However, prices are rising in line with the general food inflation trend, and poultry supplies remain vulnerable to avian flu, as well as higher feed costs.

VEGETABLES

The impact of the hot summer on produce is likely to be felt across the autumn and winter. Supplies of broccoli and cauliflower are already limited, while the combination of the heatwave and various hosepipe bans meant producers were late planting some winter crops, including carrots, parsnips and cabbage. This is likely to impact quality and availability later in the year.

POTATOES

Concerns remain about the impact of the hot summer in the coming months, which delayed the planting of winter crops. Suppliers are reporting that the UK potato crop is currently good in terms of quality and yield, but the planting delay is likely to affect price and availability later in the year and into 2026.

PORK

Pork has seen price rises, and the impact of the hot summer on feed costs is expected to push up costs further this autumn. Even so, pork is likely to be a better value option than beef or lamb for operators planning autumn and festive menus, with UK production up in response to producers getting better value.

WINE

The dry summer was good news for many fruits, including grapes, which ripened early. With UK wine producers looking for new opportunities, operators who previously found home produced wine too expensive might want to look again. UK sparkling wine is a high-quality option for festive drinks lists.

SALADS

Spain and other parts of Southern Europe were affected by the extreme heatwave and widespread wildfires across the summer. This has an impact on production of salad crops such as tomatoes, peppers, cucumber and lettuce, and with Spain the main source of UK supplies across the winter, the impact on price and availability will be felt for some time.

Inflation

The headline CPI rate of inflation in the UK was 3.8% in July, up from 3.7% a month earlier. The British Retail Consortium reported that food inflation increased to 4.2% year-on-year in August, driven by sharp price increases in staple food items such as eggs and butter.

Share this Market Forecast

- Seasonality Guide

IN SEASON

- Mussels

- Palourde Clams

- Smoked Haddock

- Mackerel

- Lemon Sole

- Coley

- Brill

- Autumn Squash

- Plums

- Apples

- Pears

- Parsnips

- Rainbow Chard

- Jerusalem Artichoke

- Kale

- Seasonality Guide

IN SEASON

- Mussels

- Palourde Clams

- Smoked Haddock

- Mackerel

- Lemon Sole

- Coley

- Brill

- Autumn Squash

- Plums

- Apples

- Pears

- Parsnips

- Rainbow Chard

- Jerusalem Artichoke

- Kale